Dealroom’s latest report on the Spanish tech scene is out! And it confirms that Spain still lags behind most western European countries when it comes to tech. However, it also shows the Spanish ecosystem is growing extremely fast, and Spanish venture capital funds (VCs) have quite an opportunity to position themselves as major players at the (pre-) seed stage. This should not be understated.

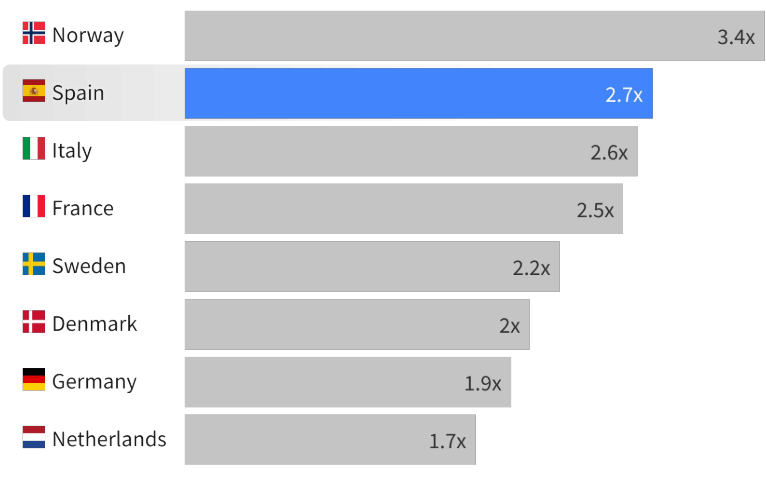

Across Europe, the UK tops the ranking – once again – followed by Germany and France. In all fairness, this is no surprise. We also see Sweden, the Netherlands, and Switzerland better positioned than Spain. Although these countries are considerably smaller than Spain, they have traditionally invested in innovation and it has led to the creation of relevant hubs in Stockholm, Amsterdam, and Zurich, respectively. In any case, the Spanish tech ecosystem is growing faster than any of these hubs, second in Europe only to Norway.

Within Spain, Madrid and Barcelona are the most prominent tech hubs, as most VCs and startups operate from there. This centralization actually leads to better interconnectivity and networking opportunities, a phenomenon seen all across Europe – Paris in France, Berlin and Munich in Germany, and Amsterdam in the Netherlands are just some prime examples. However, the Basque region and Valencia are relatively well positioned. In particular, San Sebastián and Bilbao jointly receive more VC investment per capita than Madrid, with only Barcelona ahead of them.

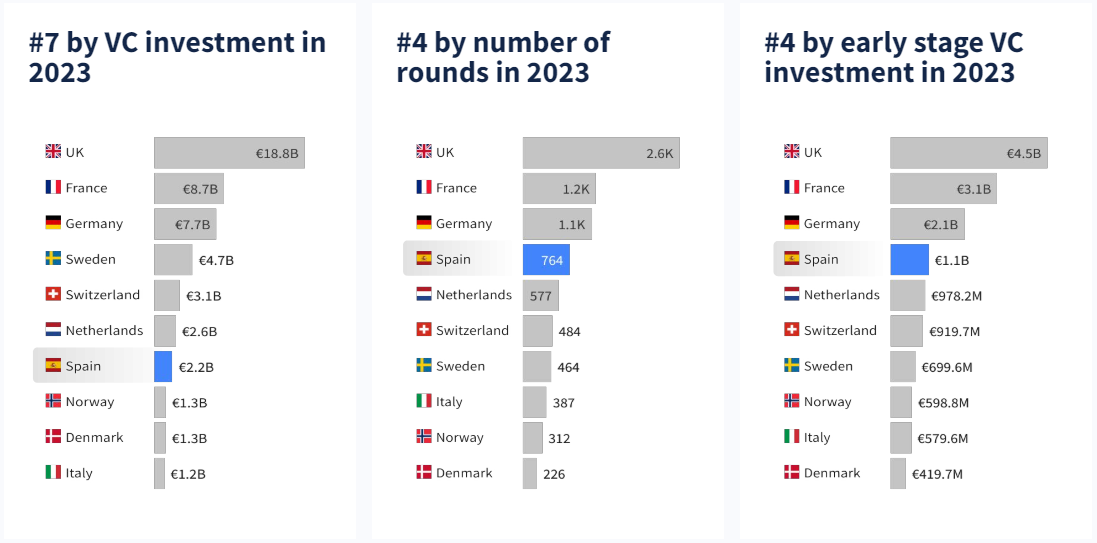

VC investment in Spain was relatively modest in 2023 (€2.2B), but it stood out in early-stage investing, as half of these investments (€1.1B) went straight to early-stage startups. This also explains the high number of investment rounds that took place in 2023, meaning that many ventures benefited from these investments. However, larger tickets (series A+) are relatively scarce in Spain, and although the current landscape provides opportunities for startups to blossom, most will eventually need to raise funds abroad if the later-stage investing landscape doesn’t improve.

Although the share of manufacturing VC investment is at a record high, most VC investment tends to go to SaaS or marketplace startups. These are typically less capital-intensive ventures with fewer challenges in terms of scalability, which can somewhat ease the funding problem. In addition, climate, biotech, and energy are the most funded sectors. This clearly shows a shift in the Spanish VC landscape towards startups with solutions that bring real impact and will not only solve today’s problems but also those of tomorrow.

Dealroom’s report also brings two other interesting topics to the table. Investment in female-founded startups has had an upward trend since 2013 although they remain somewhat marginal. According to Dealroom, only 12% of VC investment since 2019 has gone to female-founded startups. In addition, the report also mentions the current Spanish university spin-off creation. If you are interested in the topic, I would recommend reading Dealroom’s European Deep Tech 2023 report.

To sum up, Spain is stepping up in the VC and startup game, although the Spanish ecosystem won’t be able to compete against the French, Swedish, or British hubs anytime soon. While the lack of investment at a later stage may have an impact down the line, Spain has a great opportunity to position itself at the earliest part of the VC and startup curve in key sectors like health and energy.

Main picture: Jiger Panchal in Unsplash